See all press

July 3, 2026

By Shadrack Kiratu, Director of Operations, M-TIBA

At the Africa Re International Medical Insurance & Reinsurance Workshop in June 2026, we asked medical insurance executives from across the continent a simple question.

Where do you see the greatest pressure on your medical portfolio, and where do you see the biggest opportunity to improve performance?

The findings were both familiar and revealing.

The gap between pressure and opportunity

Medical inflation remains the dominant concern.

66% percent of respondents identified it as the biggest pressure on their business. Fraud, waste and abuse followed closely at 57%, highlighting that operational leakage is viewed almost as seriously as broader cost inflation.

When we shifted the discussion from pressure to opportunity, one issue moved clearly to the top.

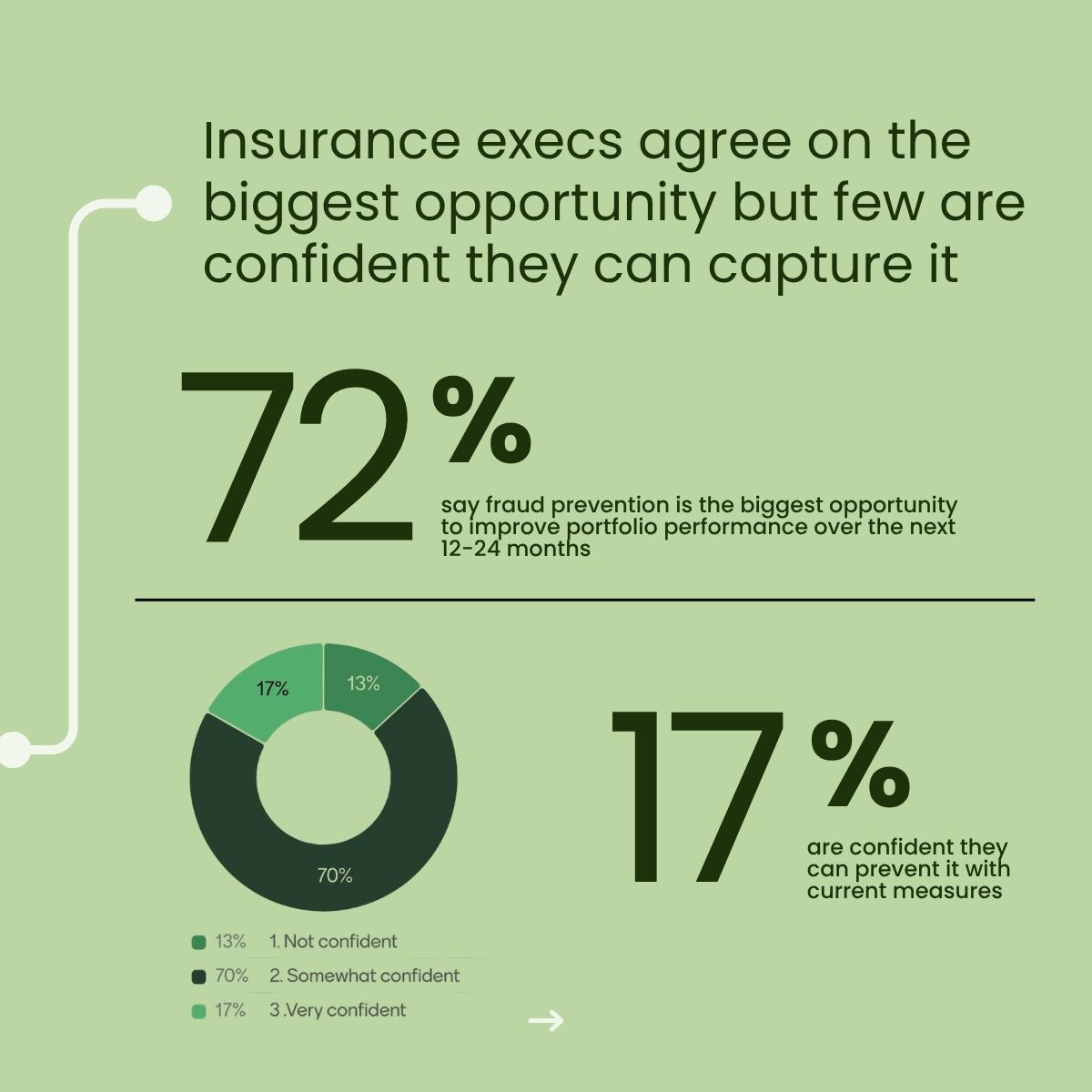

72% percent of respondents identified fraud prevention as the single biggest opportunity to improve performance over the next 12 to 24 months. Better data and analytics ranked second at 55%, followed by provider network management (43%) and member engagement (34%).

Yet confidence in mitigating this remains largely limited across the industry.

Only 17% described themselves as very confident in their ability to prevent fraud effectively. 70% percent said they were only somewhat confident, while 13% were not confident at all.

This suggests the challenge is no longer recognising the problem but rather translating that understanding into day-to-day operational control.

From our experience managing healthcare spend, this gap is rarely caused by a lack of investment in operations. Most insurers already have experienced claims teams, provider management processes and fraud investigations. The challenge is that many interventions still happen after claims have been processed and paid, when the opportunity to influence cost has already diminished.

Behaviour remains one of the hardest variables to manage

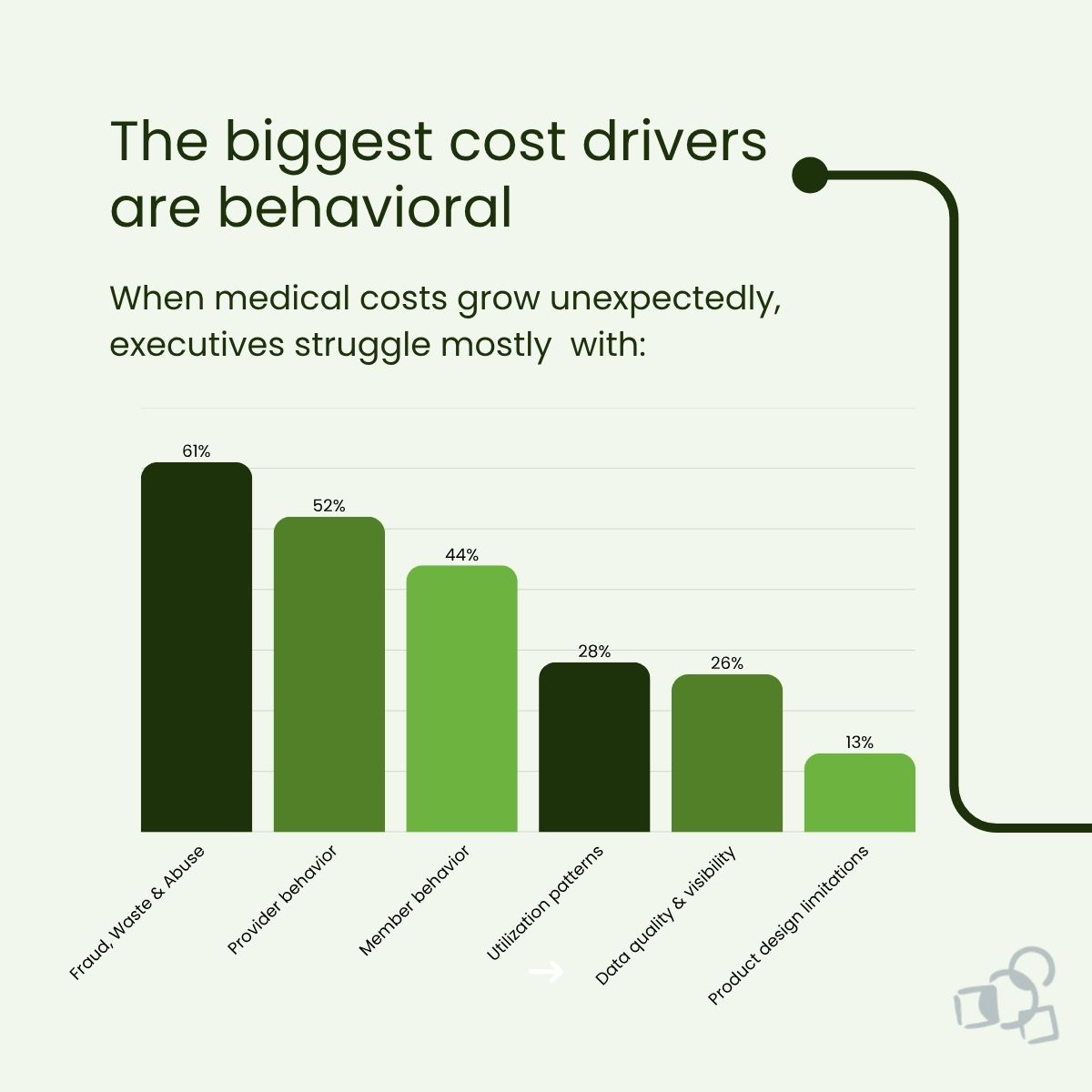

When we asked executives which factors are hardest to control as healthcare costs increase, the responses were strikingly consistent.

→ Fraud, waste and abuse: 61%

→ Provider behaviour: 52%

→ Member behaviour: 44%

These ranked ahead of utilisation patterns (28%), data quality (22%) and product design (13%).

This highlights an important reality.

Many of the largest drivers of medical costs are behavioural rather than structural. Provider billing practices, referral patterns, treatment decisions and member utilisation all influence portfolio performance.

One lesson from operating health insurance schemes at scale is that behaviour changes when incentives, transparency and operational controls improve. Consistent application of provider tariffs, clearer benefit rules and earlier identification of unusual claiming patterns all contribute to better outcomes over time.

The visibility gap

We also asked respondents how confident they were in identifying emerging claims cost trends.

Again, only 17% were very confident.

That finding matters because managing a medical portfolio depends on timely information. Delayed reporting often means management teams recognise cost deterioration weeks or months after it has already occurred.

Across the portfolios M-TIBA supports, better operational visibility has enabled insurers to move beyond retrospective reporting towards active portfolio management. That has contributed to claims adjudicated in days rather than months and claims costs reduced by 15%. That shift allows intervention while trends are still emerging, rather than after they have become embedded in results.

Visibility does not solve every problem.

It gives operational teams the opportunity to act before problems become financial results.

What this means for the industry

The survey points to a clear conclusion.

Medical inflation remains the defining challenge, but insurers increasingly see fraud, waste and abuse as the area where they have the greatest opportunity to improve performance.

Our experience suggests that sustainable improvement rarely comes from isolated fraud initiatives alone.

It comes from strengthening the operating model across the entire claims journey. Better provider management. Consistent application of medical and benefit rules. Earlier visibility into emerging trends. Stronger clinical oversight. Faster operational feedback loops.

These capabilities reinforce one another.

For insurers already under pressure on combined ratio, closing this gap isn't a compliance nicety - it's a direct, measurable lever on the loss ratio side of the equation.

The executives we spoke with are aligned on where the opportunity lies. The next stage for the industry is building operating models that allow those insights to influence decisions while care is still being delivered.

That is the operating model we've built and run — not as three separate initiatives, but as one system. If your team is working through the same gap, we're glad to compare notes.

Notes:

This article is based on a poll conducted during the Africa Re International Medical Insurance & Reinsurance Workshop held in Nairobi in June 2026. Fifty-five of seventy participating executives responded, representing a 79% response rate.

[See how M-TIBA's platform closes the fraud confidence gap → Here ]

M-TIBA is a next-generation health insurance platform and operations partner that helps insurers run profitable health portfolios with real-time data and automation across Africa.